Never too early to organize your tax documents for 2019

Although the tax deadline for filing and paying 2019 federal income taxes is still months away, it’s never too early to get organized.

On a yearly basis (usually in November) the IRS adjusts as many as 40 tax provisions for inflation. This is done to prevent what is called “bracket creep,” when people are pushed into higher income tax brackets or have reduced value from credits and deductions due to inflation, instead of any increase in real income. In some cases the changes may seem minimal, but hey – a penny saved is a penny earned!

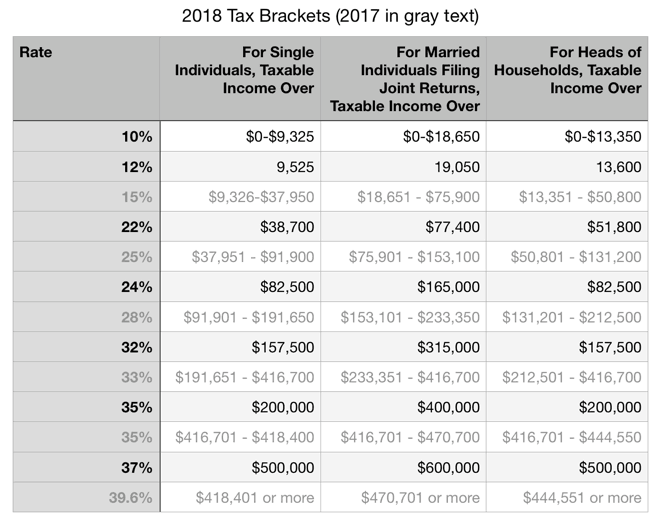

The IRS used to use the Consumer Price Index (CPI) to calculate the past year’s inflation. However, with the Tax Cuts and Jobs Act of 2017, the IRS will now use the Chained Consumer Price Index (C-CPI) to adjust income thresholds, deduction amounts, and credit values accordingly. Below see the updated tax brackets for 2019.

Income Tax Brackets and Rates

In 2019, the income limits for all tax brackets and all filers will be adjusted for inflation and will be as follows (Tables 1). The top marginal income tax rate of 37 percent will hit taxpayers with taxable income of $510,300 and higher for single filers and $612,350 and higher for married couples filing jointly.

| Rate | For Unmarried Individuals, Taxable Income Over | For Married Individuals Filing Joint Returns, Taxable Income Over | For Heads of Households, Taxable Income Over |

|---|---|---|---|

| 10% | $0 | $0 | $0 |

| 12% | $9,700 | $19,400 | $13,850 |

| 22% | $39,475 | $78,950 | $52,850 |

| 24% | $84,200 | $168,400 | $84,200 |

| 32% | $160,725 | $321,450 | $160,700 |

| 35% | $204,100 | $408,200 | $204,100 |

| 37% | $510,300 | $612,350 | $510,300 |

Standard Deduction and Personal Exemption

The standard deduction for single filers will increase by $200 and by $400 for married couples filing jointly (Table 2).

The personal exemption for 2019 remains eliminated.

| Filing Status | Deduction Amount |

|---|---|

| Single | $12,200 |

| Married Filing Jointly | $24,400 |

| Head of Household | $18,350 |