Despite the ongoing government shutdown, Office of Management and Budget Director Russell Vought issued a statement yesterday that tax refunds will go out as scheduled, unlike in previous shutdowns. The Internal Revenue Service has given the green light to processing returns as it set the date to being accepting returns beginning Jan 28th.

IRS Commissioner Chuck Rettig said on Monday, “we are committed to ensuring that taxpayers receive their refunds notwithstanding the government shutdown. I appreciate the hard work of the employees and their commitment to the taxpayers during this period.” The IRS doesn’t normally issue refunds during a shutdown, however Rettig said the IRS has “consistently been of the view that it has the authority to pay refunds despite a lapse in annual appropriations.”

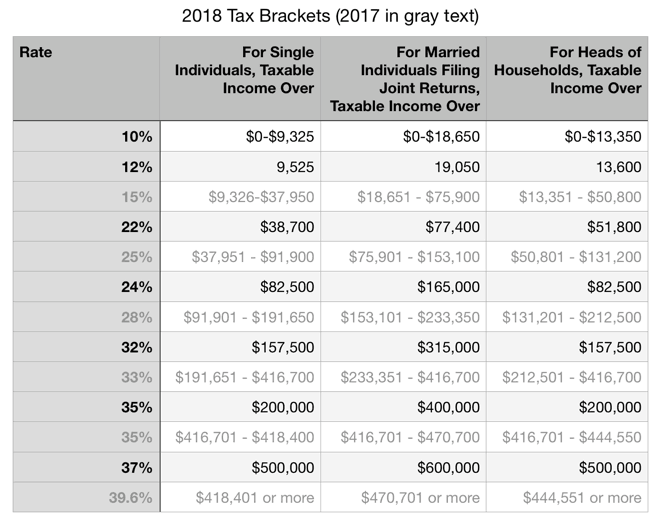

The IRS closure during the partial government shutdown couldn’t have come at worse time for taxpayers looking for answers to the changes brought about by the Tax Cuts and Jobs Act of 2017 signed by President Donald Trump on Dec. 20, 2017. With almost 90% of the IRS workforce on furlough it’s unlikely that many taxpayers will be able to reach the IRS for help during the ongoing shutdown.

The filing deadline to submit 2018 tax returns is Monday, April 15 for most taxpayers. Taxpayers in in Maine and Massachusetts are granted a couple of extra days due to the Patriots’ Day holiday on April 15, likewise those residing in the District of Columbia where Emancipation Day holiday is being observed on April 16 also do not have to file until April 17th.