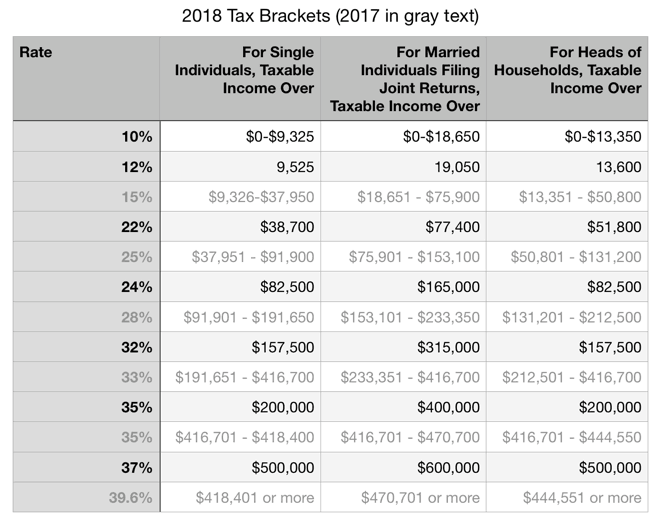

2018 Estate Planning

Most of the media coverage and attention on the new tax code, The Tax Cuts and Jobs Act (TCJA), have been focused on changes to income taxes (individual and corporate) and their respective brackets. Although the new law did not “repeal” the Federal Estate Tax, it does include some provisions that could impact some tax payers and their estate planning.

Exemption Increases

The biggest change in the new tax code regarding estate planning is that it more than doubles the exemption amounts for gift and estate tax exemptions and the generation-skipping transfer (GST) tax exemption, from $5.49 million for 2017 to $11.18 million (or $20 million for married couples with proper planning) for 2018. The top marginal rate for all three taxes remains at 40% — only three percentage points higher than the top income tax rate.

This is good news for those with large estates, however absent congressional action, the exemptions will revert to their 2017 levels (adjusted for inflation) in 2026. Although these “doubled exemption” amounts only affect a small population of taxpayers, it is important for those with estates in the roughly $6 million to $11 million range (double that for married couples) to consider making tax-free asset and wealth transfers prior to 2026 when the higher exemption amounts are set to expire.

It is important to consider however for taxpayers not affected by the above exemption amounts it may behoove them to hold assets until death. Specifically, when a a taxpayer gives away an appreciated asset the recipient takes over their tax basis in the asset which would trigger a capital gains tax should the recipient turnaround and sell it. On the contrary, when an appreciated asset is inherited, the recipient’s basis is “stepped up” to the asset’s fair market value on the date of death, which could significantly reduce (or even erase) the capital gain. Hence, retaining appreciating assets for taxpayers with estates less than $11 million ($22 million for married couples) can you save your heirs a significant amount of income taxes.

It is also important to keep in mind that some states have their own estate taxes whose exemption amounts are almost always lower than the federal amounts.

Updates to Section 529 plans

Another key change brought with the new tax code has been the expansion in tax benefits for 529 plans. Many tax professionals have long been proponents for families using 529 plans to grow money tax-free for their children’s education. Previously, 529 plans could only be used for eligible colleges and universities, but the TCJA now allows them for private, public, and religious kindergarten through 12th grade – up to $10,000 per year per child. This lucrative savings method for families can also be extended to other relatives like grandparents who can pare down their estates by making contributions to 529 plans while benefiting their grandchildren and their education.

The complexity of estate planning can be a daunting task for even the most sophisticated taxpayer, therefore it is always a good idea to consult a tax professional like those found at TaxPM who can help you review, and if necessary revise your estate planning strategies.